Sophisticated Pricing Builds Competitive Products — ③: Nested Scenario Modeling

Authored by Jihyun Kim, Global Sales Executive RNA Analytics

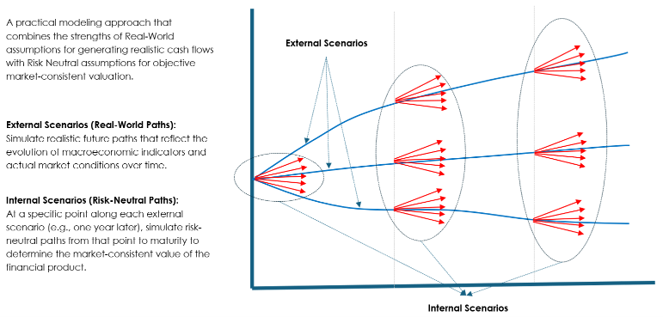

Nested Scenario Modeling

In the previous installment, we discussed the problems of examining only the CSM metric when pricing insurance products, and the need for a shareholder-profit-perspective pricing metric. We noted that the concept of traditional VNB is useful as a way to evaluate distributable earnings — a shareholder-profit concept — but that it cannot be used as is and must be improved to fit the requirements of the current regime.

Why can traditional VNB based on the TEV methodology not be used as is in the IFRS 17 and K-ICS environment?

The most important reason is that traditional VNB is a deterministic valuation approach on a Real-World (RW) basis, whereas the basis for computing reserves and capital under IFRS 17 and K-ICS is Risk-Neutral (RN) valuation. In computing VNB, reserves and capital are calculated at each future point over the projection period in order to derive distributable earnings; accordingly, a modeling logic must be built that values these at each point on a current-value basis under the Risk-Neutral standard, in accordance with the IFRS 17 and K-ICS regimes.

In addition, a major limitation frequently cited for traditional VNB is that a real-world deterministic valuation cannot adequately value the cost of options and guarantees embedded in insurance contracts. Because options and guarantees constitute a significant portion of insurance-contract valuation — and are especially high-volatility items under IFRS 17 current valuation as market variables change — their valuation must not be overlooked. To value the cost of embedded options and guarantees in a way that is consistent with financial-market option-valuation methods and aligned with IFRS 17 standards, valuation must be done using Risk-Neutral stochastic scenarios. To appropriately reflect the cost of options and guarantees in the VNB projection, one must apply not only real-world scenarios but also Risk-Neutral stochastic scenarios for computing option/guarantee costs at every future point of the projection.

Ultimately, the way to appropriately use the VNB metric under IFRS 17 and K-ICS is to implement a model structure in which, at each future point projected under real-world scenarios, liabilities, capital, and option/guarantee costs are computed on the basis of Risk-Neutral scenarios. The method for solving this problem is to adopt “Nested Scenario” modeling.

To introduce the basic concept of Nested Scenario modeling: it is a simulation-based valuation approach that nests real-world scenarios and Risk-Neutral scenarios, and it has long been adopted in advanced insurance markets such as North America. Scenarios reflecting real-world expectations for how macroeconomic and market indicators change over time are generated, and at each point (node) of a real-world scenario, Risk-Neutral scenarios are again generated to value liabilities and capital. Applying stochastic scenarios also makes it possible to appropriately compute the cost of embedded options and guarantees. The Nested Scenario modeling methodology is useful because it computes and reflects the value of insurance products and the cost of embedded options and guarantees in accordance with financial-market pricing methodology, while still allowing views on changes in the economic environment and the effects of future management strategy to be reflected.

《Structure of Nested Scenario Modeling》

Sophisticated pricing based on Nested Scenario modeling becomes a powerful tool that overcomes the twin constraints of the IFRS 17/K-ICS regime environment and an intensified market-competition environment, and that confers strategic competitive advantage in product and pricing decisions.

First, under IFRS 17 and K-ICS in particular, pricing decisions must be grounded in sufficient and sophisticated analysis of the impact of product sales on the company’s profit and required capital. Before IFRS 17 and K-ICS, the point at which the impact of product sales was reflected in profit and required capital was not immediate, so there was arguably a strong tilt toward the sales-volume perspective in the industry’s product-pricing decisions, with insufficient assessment of financial impact. Under the current framework, with IFRS 17 and K-ICS in force, the impact of product sales on profit and capital is reflected immediately after sale, and the difference between pricing assumptions and actual experience is likewise reflected as soon as it is observed. If a product sold without sufficient review of its profit and capital impact later becomes a problem, that problem — unlike in the past — is not in the distant future but is reflected immediately in the company’s financial position, and can put the management that made the sales decision in the difficult position of being held directly accountable. In particular, under the current regime based on Risk-Neutral valuation, product profitability and required capital vary substantially with changes in economic variables. It is therefore essential to properly perform, at the pricing stage, sensitivity analyses that consider a range of future scenarios and the valuation of guarantees, so that product profitability and the company’s financial position remain sound even under changes in key variables.

Second, as dependence on external distribution channels has deepened, product competition among insurers has become extremely fierce. Insurers must now make attractive product proposals to win the choice of their distribution partners. The elements of an “attractive product” proposal that persuades a distributor are aggressive benefits, low prices, high commissions, or some combination of these. Meeting these requirements, one comes to face a situation in which it is all but impossible to obtain profitability-analysis results that meet the required standards using simple methodologies and conservative assumptions. It has become impossible to launch a competitive product by pricing with a roughly simple, conservative methodology. One can neither give up product competitiveness nor launch a precarious product that may soon prove to be a loss-making contract. It is at this juncture that the pricing capability to find and bore into narrow pockets of opportunity through fine-grained analysis becomes the key that separates companies’ competitiveness. Through Nested Scenario modeling, one can find the range of product designs whose profitability holds up even when reflecting a variety of future scenarios; and for product configurations that pass pricing validation and meet the company’s own risk-tolerance level, one can confidently drive sales and lead the company’s profitable growth. Ultimately, sharpening the focus of product proposals through more sophisticated pricing analysis is a proactive strategy that creates opportunity, and a weapon that delivers victory in competition.

Third, in today’s fierce competitive environment, it is difficult to find profitable opportunities through simple static pricing modeling alone. A passive approach that mechanically calculates and confirms product profitability under given conditions has clear limitations in finding areas of opportunity. In response, pricing can proactively pursue opportunity by integrating a dynamic management strategy — one that responds nimbly to environmental change — into pricing logic based on Nested Scenario modeling. This, too, is important, because it renders in numbers, within the pricing results, the value that management’s dynamic decisions create.

The Nested Scenario modeling technique is more complex than the conventional single-scenario approach, but it is nonetheless an advanced framework that should be adopted as quickly as possible — because the pricing-victory opportunity that its sophisticated analysis provides will drive management success in the fiercely competitive insurance industry.